Page 170 - GHES-2-2

P. 170

Global Health Econ Sustain An analysis of national economic resilience

Q4 2019 to 2.45% in Q1 2020. This uptick can be attributed

to their primary clientele – small and microenterprises,

which were disproportionately affected by the epidemic.

Conversely, the other three bank types, typically averse

to lending to higher-risk small and micro enterprises,

maintained higher asset quality and were less affected by

the epidemic. However, as the epidemic became gradually

controlled and the businesses resumed normal operations,

the NPL rate began to decrease, stabilizing after Q3 2020.

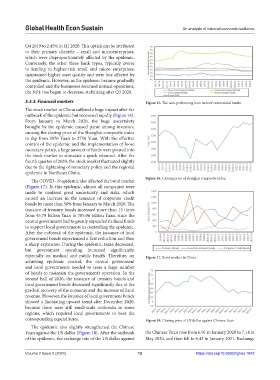

5.3.3. Financial markets Figure 15. The non-performing loan ratio of commercial banks

The stock market in China suffered a huge impact after the

outbreak of the epidemic but recovered rapidly (Figure 16).

From January to March 2020, the huge uncertainty

brought by the epidemic caused panic among investors,

causing the closing price of the Shanghai composite index

to dip from 2976 Yuan to 2750 Yuan. With the effective

control of the epidemic and the implementation of loose

monetary policy, a large amount of funds were poured into

the stock market to stimulate a quick rebound. After the

fourth quarter of 2020, the stock market fluctuated slightly

due to the tightening of monetary policy and the regional

epidemic in Northeast China.

Figure 16. Closing price of shanghai composite index

The COVID-19 epidemic also affected the bond market

(Figure 17). In this epidemic, almost all companies were

made to confront great uncertainty and risks, which

caused an increase in the issuance of corporate credit

bonds by more than 50% from January to March 2020. The

issuance of treasury bonds increased more than 15 times

from 45.79 billion Yuan to 785.06 billion Yuan, since the

central government had to greatly expanded its fiscal funds

to support local governments in controlling the epidemic.

After the outbreak of the epidemic, the issuance of local

government bonds experienced a first reduction and then

a sharp expansion. During the epidemic, taxes decreased,

but government spending increased significantly,

especially on medical and public health. Therefore, on Figure 17. Bond market in China

achieving epidemic control, the central government

and local governments needed to issue a large number

of bonds to maintain the government’s operation. In the

second half of 2020, the issuance of treasury bonds and

local government bonds decreased significantly due to the

gradual recovery of the economy and the increase of fiscal

revenue. However, the issuance of local government bonds

showed a fluctuating upward trend after December 2020,

because there were still small-scale outbreaks in some

regions, which required local governments to bear the

corresponding expenditures. Figure 18. Closing price of US dollar against Chinese Yuan

The epidemic also slightly strengthened the Chinese

Yuan against the US dollar (Figure 18). After the outbreak the Chinese Yuan rose from 6.91 in January 2020 to 7.14 in

of the epidemic, the exchange rate of the US dollar against May 2020, and then fell to 6.43 in January 2021. Exchange

Volume 2 Issue 2 (2024) 12 https://doi.org/10.36922/ghes.1842